A Complete Guide to Medicare Advantage Plans and Choosing the Right Provider

Medicare Advantage (Part C) is an alternative to Original Medicare that bundles the coverage of Part A (hospital insurance) and Part B (medical insurance), and often includes additional benefits like prescription drug coverage. As more seniors look for comprehensive healthcare solutions, understanding how Medicare Advantage works and how to choose the best plan for your needs is essential. This guide will walk you through everything you need to know.

What Is Medicare Advantage?

Medicare Advantage, also known as Medicare Part C, is an all-in-one plan offered by private insurance companies that contract with Medicare. These plans provide all the benefits of Original Medicare (Part A and Part B) and often include extra perks, such as prescription drug coverage (Part D), vision, dental, and hearing care.

In 2025, Medicare Part D will have a $2,000 out-of-pocket spending limit for prescription drugs, which means once you reach that threshold, you won’t need to pay any more for covered medications.

How Do Medicare Advantage Plans Work?

Medicare Advantage plans are administered by private insurers, who receive a payment from Medicare to manage the coverage. These plans operate similarly to employer-sponsored health insurance, where you pay a monthly premium in addition to your Part B premium. You’ll also pay set copays, coinsurance, and deductibles for different types of care.

However, there are some important rules to keep in mind:

• Network restrictions: You must use the plan's network providers, except in emergencies or for urgent care outside the service area.

• Prior authorizations: Many services, such as hospital stays and certain procedures, require prior approval.

Choosing the right provider involves understanding the details of what’s covered and whether your preferred doctors and hospitals are included in the plan's network.

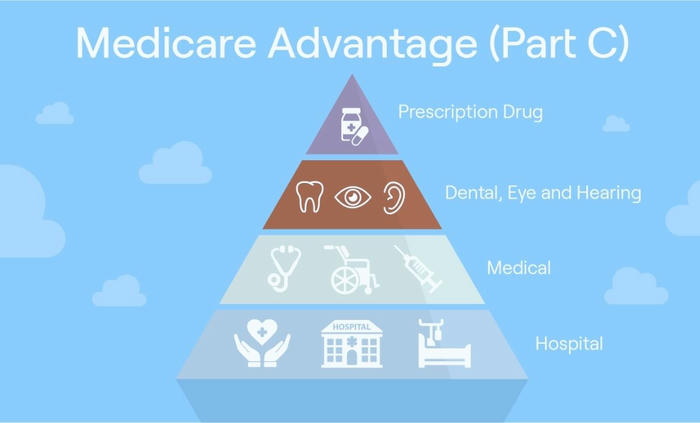

What Do Medicare Advantage Plans Cover?

All Medicare Advantage plans must cover everything that Original Medicare provides, including:

• Hospital inpatient care (Part A)

• Skilled nursing facility care

• Hospice care

• Home health care

• Ambulance services

• Durable medical equipment (e.g., wheelchairs, oxygen)

• Mental health services (both inpatient and outpatient)

• Limited outpatient prescription drugs (Part D)

Beyond that, many Medicare Advantage plans offer additional benefits:

•Prescription drug coverage (Part D)

•Vision, dental, and hearing care

•Fitness program memberships (e.g., gym access)

•Transportation for medical visits

•Over-the-counter drug coverage

These additional benefits can be a game-changer for people who need more than just basic healthcare coverage.

Who Should Get a Medicare Advantage Plan?

Medicare Advantage plans are a great choice for:

•Those who want a bundled health plan: If you’re looking for a single plan that covers hospital stays, doctor visits, prescription drugs, and sometimes extra perks like vision and dental, Medicare Advantage is a good option.

•Individuals who take prescription drugs: Most Medicare Advantage plans include prescription drug coverage, which could be beneficial for those who need regular medications.

•People who need comprehensive care: If you need more than just basic healthcare services, the added benefits of Medicare Advantage may provide the coverage you're looking for.

Who Shouldn’t Get a Medicare Advantage Plan?

Medicare Advantage may not be suitable for those who:

•Prefer to manage their benefits separately: If you prefer handling your Part A, Part B, and Part D coverage individually, you may prefer Original Medicare.

•Use out-of-network providers: Medicare Advantage requires you to use network providers for non-emergency care. If your doctor or specialist isn't in-network, you may face higher out-of-pocket costs or have to pay for care out of pocket.

•Need specific treatments that require prior authorizations: Some Medicare Advantage plans may require you to get approval for certain treatments and services, which could cause delays or additional paperwork.

In such cases, you may find that Medigap or Original Medicare with a Part D plan better suits your needs.

How to Sign Up for Medicare Advantage During Open Enrollment

You can enroll in a Medicare Advantage plan during two key enrollment periods:

•Initial Enrollment: If you're newly eligible for Medicare (turning 65 or qualifying for disability), you can enroll during the 7-month period that includes the month you turn 65.

•Annual Enrollment: From October 15 to December 7 each year, you can sign up, switch, or drop a Medicare Advantage plan. Your new coverage will start on January 1.

If you’re already enrolled in Medicare Advantage, you can switch plans or revert to Original Medicare during the Medicare Advantage Open Enrollment period, from January 1 to March 31.

When Will 2025 Medicare Advantage Plans Be Available?

The Medicare Advantage plans for 2025 will be available starting October 15, 2024. You can browse available plans at Medicare.gov, compare coverage, and make your selection. Remember that the Annual Enrollment Period is your opportunity to review your options and make changes if necessary.

How Much Does Medicare Advantage Cost?

The cost of Medicare Advantage plans varies widely depending on the plan, location, and coverage options. Here are some key factors to consider:

•Monthly premium: Some Medicare Advantage plans charge a $0 premium, but others may have a premium in addition to your Part B premium.

•Copayments and coinsurance: Most plans charge copays for doctor visits and hospital stays. You’ll want to check the copay rates before signing up.

•Deductibles: Some plans have an annual deductible, which is the amount you must pay before your plan starts covering costs.

•Out-of-pocket limits: Medicare Advantage plans have an annual out-of-pocket maximum, after which the plan pays 100% of covered services. The limits vary by plan.

To find out how much a specific plan will cost, you can use the tools at Medicare.gov to compare options available in your area.

Different Types of Medicare Advantage Plans

There are several types of Medicare Advantage plans, each with its own rules and benefits:

Health Maintenance Organization (HMO): Requires you to use a network of doctors and hospitals and may require referrals to see specialists.

Preferred Provider Organization (PPO): Offers more flexibility in choosing healthcare providers, but costs more if you go outside the network.

Private Fee-for-Service (PFFS): Allows you to see any provider who agrees to the plan’s terms, but the plan may not cover all providers.

Special Needs Plans (SNP): Tailored for individuals with specific conditions like chronic diseases or disabilities. Coverage is customized to meet the needs of these groups.

Medicare Advantage vs. Original Medicare: What’s the Difference?

The primary difference between Medicare Advantage and Original Medicare is the way the coverage is structured. Original Medicare consists of Part A (hospital) and Part B (medical), but it doesn’t offer extra benefits like dental, vision, or prescription drugs unless you purchase additional coverage. Medicare Advantage plans, on the other hand, offer all these benefits bundled together in one plan.

Medicare Advantage vs. Medicare Supplement (Medigap): What’s the Difference?

Medicare Supplement (Medigap) plans are designed to fill the gaps in Original Medicare, helping to cover things like deductibles and coinsurance. Medigap plans don’t offer prescription drug coverage, so if you need that, you’d have to enroll in Part D separately.

In contrast, Medicare Advantage plans replace Original Medicare and often include drug coverage and extra benefits, like dental or vision.

The Pros and Cons of Medicare Advantage Plans

Pros:

1.Comprehensive coverage in one plan (Part A, B, D)

2.Additional benefits like dental, vision, and hearing

3.Lower monthly premiums for some plans

Cons:

1.Limited choice of healthcare providers (must use the plan's network)

2.Prior authorization may be required for certain services

3.Plans and costs can vary significantly by location

How to Find the Best Medicare Advantage Plans in 2024

Finding the right Medicare Advantage plan can be overwhelming, but the right plan is out there. Joe Valenzuela, a health insurance expert, recommends starting by identifying your healthcare needs and priorities. Speak with a knowledgeable insurance agent who can help guide you through the process and explain the fine print. It’s also important to compare premiums, copayments, out-of-pocket costs, and prescription drug coverage before making your decision.

Understanding the ins and outs of Medicare Advantage plans can help you make an informed decision that best suits your healthcare needs and budget. Take the time to research your options, and don’t hesitate to seek professional advice to ensure you’re selecting the plan that’s right for you.